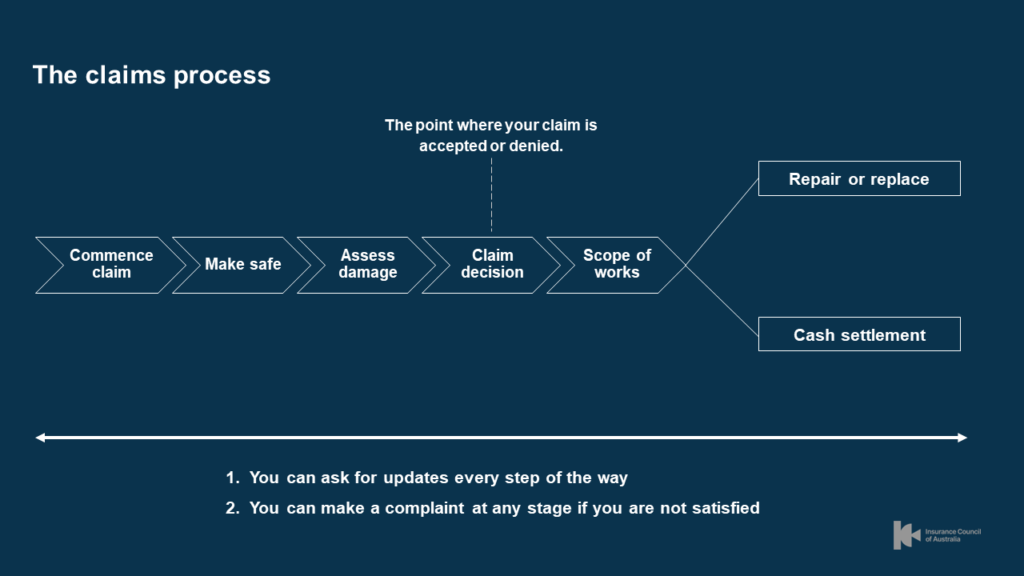

What do I need to provide to make a Business Interruption claim?

Many businesses may have Business Interruption (BI) cover in their business insurance policies. Each policy varies according to the business, but in general BI is designed to cover a loss of profit while a business cannot operate due to certain insured events, for example the closure of premises by a public authority.

Your broker or insurer will be able to advise you whether you have a BI policy and if so, whether it may cover the losses you have incurred while your business was closed. If you do have a BI claim you will have to submit financial documentation to evidence the financial loss your business has suffered. In most instances, the product disclosure statement (PDS) that was provided to you when you bought the policy outlines the information which your insurer needs to assess a BI claim.

The Insurance Council of Australia has collated the list set out below to assist BI policyholders when making a claim. This list provides a general outline of the documents and information required to submit a BI claim.

As each claim is different insurers may also require additional or different information, depending on factors such as the period of time that a business has been impacted, the nature of the business and the type of loss suffered. In particular you should be prepared to provide financial information not just for the last year but for previous years.

If you consider that you may have a BI claim it is important to start gathering the relevant financial information as soon as possible. Putting this information together when it is at hand will assist the claims process and help your insurer establish BI losses. Your broker or insurer can also help you identify the documents and information you need to collate.

Documents required

- Historical BAS Lodgements with ATO receipts for the last year to verify the gross profit.

- Historical Financial Year Profit and Loss Statements including detailed trading account summary for the last year. You may be able to produce this from a Management Information System used for bookkeeping such as MYOB, QuickBooks or Xero.

- If available Historical Quarterly Profit and Loss Statements for the last year.

- If available Historical Monthly Profit and Loss Statements for the last year.

- If necessary and available Historical weekly trading figures.

- Evidence of payroll costs (in the event that your policy covers payroll).

- Copy of any correspondence between the Insured/Landlord regarding the waiver, deferment or abatement of any rent during the interruption period.

- Lease Agreement (if applicable)

- Franchise Agreement (if applicable)

Information required

- Provide details of when your business was closed and why.

- Provide details of your business' normal daily/weekly trading hours.

- Provide details of whether your business was ordered to close or to alter its operations by a government authority (such as the Police) or Local Council.

- Provide details of whether your business was able to operate even in a reduced capacity.

- Provide details of any government grants or other financial support received.