Severe Weather

East Coast flood event insurance update – 2 March

East Coast flood event insurance update – 2 March

News release

Wednesday, 2 March 2022

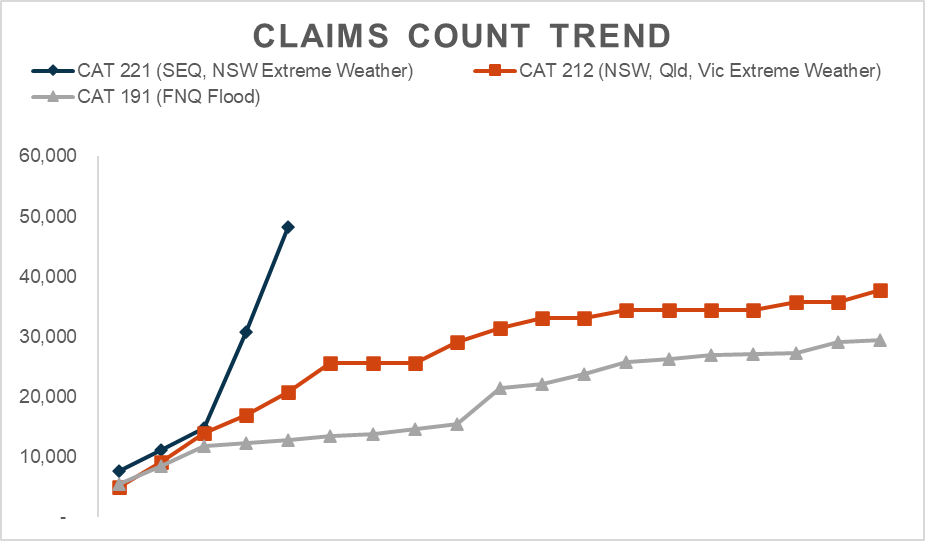

The Insurance Council of Australia (ICA) today said insurers have received 48,220 claims related to the flooding in South-East Queensland and the New South Wales coast.

This is a 53 per cent increase on yesterday’s claims count and demonstrates the significant impact of this event. (see graph below)

37,807 of these claims are from Queensland, with the remainder from New South Wales. New South Wales figures are expected to increase in coming days as more policyholders return to their homes and businesses.

Eight-four per cent of total claims relate to property, with the remainder motor vehicle. Insurers do not have an estimate of claims costs at this time.

ICA CEO Andrew Hall is in Brisbane today meeting with State and Federal Government stakeholders to report on insurers’ activity and to ensure the recovery process fully supports impacted communities.

This has included discussion of the availability and affordability of flood cover.

The ICA has been working with members to conduct an aerial survey of the impacted zones to prepare high-resolution imagery of the event.

Commencing today an aerial survey will be undertaken of Lismore, Ballina, Grafton, Murwillumbah, Gympie, Maryborough, Brisbane and Logan.

The overall aim of this program is to:

- Verify the impact and scale of the event

- Improve the response time of insurers through accurate assessment of property conditions

- Work collaboratively with Government response and recovery agencies by providing them with access to the captured images

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

Following the 2011 Brisbane floods insurance policies now have a standard flood definition.

If a policyholder has opted out of flood they are most likely still covered for storm damage, and if they are unsure they should speak with their insurer.

Insurance prices risk, and that means that for those in flood-prone locations, particularly small businesses, flood cover can be costly.

That is why the ICA has called on all Australian governments to do more to protect homes, businesses, and communities from the impacts of extreme weather.

With appropriate mitigation infrastructure and household-level programs, property can be better protected and premiums can decrease, but this can only be achieved if governments act with urgency.

Remember

- Safety is the priority – don’t do anything that puts anyone at risk

- Only return to your property when emergency services give the go ahead

- If water has entered the property, don't turn on your electricity until it has been inspected by an electrician

- Contact your insurance company as soon as possible to lodge a claim and seek guidance on the claims process

- Property owners who have sustained roof damage should advise their insurer, your insurer will arrange emergency works to minimise any hazards and prevent further damage. This can include isolating damaged solar panels or electrical circuits and installing a roof tarp

- Don’t worry if you can’t find your insurance papers – insurers have electronic records and need only your name and address

What to do if your property has been impacted by flooding and storms

- You can start cleaning up but first take pictures or videos of damage to the property and possessions as evidence for your claim

- Keep samples of materials and fabrics to show your insurance assessor

- Remove water damaged goods from your property that might pose a health risk, such as saturated carpets and soft furnishings

- Make a list of each item damaged and include a detailed description, such as brand, model, and serial number if possible

- If water has entered the property, do not turn on your electricity until it has been inspected by an electrician

- Store damaged or destroyed items somewhere safe where they do not pose a health risk

- Speak to your insurer before you attempt or authorise any building work, including emergency repairs, and ask for the insurer’s permission in writing. Unauthorised work may not be covered by your policy

- Do not throw away goods that could be salvaged or repaired

East Coast flood event insurance update – 1 March

East Coast flood event insurance update – 1 March

News release

Tuesday, 1 March 2022

The Insurance Council of Australia (ICA) today said insurers have received almost 31,000 claims related to the ongoing flood emergency in South-East Queensland and the New South Wales coast.

This is a 107 per cent increase on yesterday’s claims count and is a much more significant rise at this point than was seen following last year’s floods in New South Wales and South-East Queensland (see graph over).

It is too soon to provide an estimate of claims costs given the event is still unfolding and claims are still being reported.

Given the scale of the extreme weather event insurers are closely monitoring the availability of temporary accommodation for displaced residents.

The ICA continues to engage with local governments and the Queensland, New South Wales and Federal Governments to ensure any issues identified can be managed immediately.

The ICA declared an Insurance Catastrophe for South-East Queensland on Saturday, and yesterday extended that declaration to include those areas of New South Wales impacted by the weather event that is now making its way down the coast.

Under the ICA’s Catastrophe declaration:

- Claims from affected policyholders are given priority by insurers

- Claims are triaged to direct urgent assistance to the worst-affected property owners

- An industry taskforce has been established to identify and address issues arising from this extreme weather event

- ICA representatives will be mobilised to work with local agencies and services and affected policyholders as soon as emergency services say it is safe to do so

- Insurers will mobilise disaster response specialists to assist affected customers with claims and assessments as soon as emergency services say it is safe to do so

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

Personal safety continues to be the number one priority, please follow the directions of the authorities.

This is still a large-scale unfolding event across two States with significant increases in claim numbers, and we expect this to continue to climb as people are allowed to return to their homes and businesses.

Insurers are already on-the-ground helping with claims where it is safe to do so.

I want to be clear that following the 2011 Brisbane floods insurance policies now have standard flood definitions, and if policyholders have selected that cover this will include water that is released from a dam.

Remember

- Safety is the priority – don’t do anything that puts anyone at risk

- Only return to your property when emergency services give the go ahead

- If water has entered the property, don't turn on your electricity until it has been inspected by an electrician

- Contact your insurance company as soon as possible to lodge a claim and seek guidance on the claims process

- Property owners who have sustained roof damage should advise their insurer, your insurer will arrange emergency works to minimise any hazards and prevent further damage. This can include isolating damaged solar panels or electrical circuits and installing a roof tarp

- Don’t worry if you can’t find your insurance papers – insurers have electronic records and need only your name and address

What to do if your property has been impacted by flooding and storms

- You can start cleaning up but first take pictures or videos of damage to the property and possessions as evidence for your claim

- Keep samples of materials and fabrics to show your insurance assessor

- Remove water damaged goods from your property that might pose a health risk, such as saturated carpets and soft furnishings

- Make a list of each item damaged and include a detailed description, such as brand, model, and serial number if possible

- If water has entered the property, do not turn on your electricity until it has been inspected by an electrician

- Store damaged or destroyed items somewhere safe where they do not pose a health risk

- Speak to your insurer before you attempt or authorise any building work, including emergency repairs, and ask for the insurer’s permission in writing. Unauthorised work may not be covered by your policy

- Do not throw away goods that could be salvaged or repaired

Insurance Catastrophe declaration extended to NSW

Insurance Catastrophe declaration extended to NSW

News release

Monday, 28 February 2022

The Insurance Council of Australia (ICA) has today extended the Insurance Catastrophe declaration made on Saturday for South-East Queensland to include those areas of New South Wales impacted by this weather event and the weather cell impacting south to the Mid-North Coast.

Since 21 February insurers have received almost 15,000 claims from policyholders related to extreme rainfall in both States, a 33 per cent increase on yesterdays’ claims figures.

It is too soon to provide an estimate of claims costs given the event is still unfolding and claims are still being reported.

The ICA’s Catastrophe declaration serves to escalate and prioritise the insurance industry’s response for affected policyholders.

Under the Catastrophe declaration:

- Claims from affected policyholders are given priority by insurers

- Claims are triaged to direct urgent assistance to the worst-affected property owners

- An industry taskforce has been established to identify and address issues arising from this extreme weather event

- ICA representatives will be mobilised to work with local agencies and services and affected policyholders as soon as emergency services say it is safe to do so

- Insurers will mobilise disaster response specialists to assist affected customers with claims and assessments as soon as emergency services say it is safe to do so

The extended Insurance Catastrophe declaration covers claims related to the ongoing severe weather and flooding events impacting the east coast.

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

Personal safety should be the number one priority as this extreme weather event continues to impact communities along the east coast.

It’s too early to estimate the insurance damage bill as many property owners remain in evacuation centres and flood waters continue to rise in many areas, or in others recede slowly.

The insurance industry expects the number of claims to rise significantly as policyholders return to their homes and businesses.

Insurers are already assisting policyholders, and stand ready to provide on-the-ground assistance as soon as it is safe to do so.

Remember

- Safety is the priority – don’t do anything that puts anyone at risk

- Only return to your property when emergency services give the go ahead

- If water has entered the property, don't turn on your electricity until it has been inspected by an electrician

- Contact your insurance company as soon as possible to lodge a claim and seek guidance on the claims process

- Property owners who have sustained roof damage should advise their insurer, your insurer will arrange emergency works to minimise any hazards and prevent further damage. This can include isolating damaged solar panels or electrical circuits and installing a roof tarp

- Don’t worry if you can’t find your insurance papers – insurers have electronic records and need only your name and address

What to do if your property has been impacted by flooding and storms

- You can start cleaning up but first take pictures or videos of damage to the property and possessions as evidence for your claim

- Keep samples of materials and fabrics to show your insurance assessor

- Remove water damaged goods from your property that might pose a health risk, such as saturated carpets and soft furnishings

- Make a list of each item damaged and include a detailed description, such as brand, model, and serial number if possible

- Store damaged or destroyed items somewhere safe

- Speak to your insurer before you attempt or authorise any building work, including emergency repairs, and ask for the insurer’s permission in writing. Unauthorised work may not be covered by your policy

- Do not throw away goods that could be salvaged or repaired

Insurers to meet virtually with storm affected Gippsland and Yarra Ranges locals

Insurers to meet virtually with storm affected Gippsland and Yarra Ranges locals

News release

Monday, 10 January 2022

The Insurance Council of Australia (ICA) will host virtual one-on-one consultations for Gippsland and Yarra Ranges policyholders affected by the June 2021 severe weather event. The virtual video or phone consultations can be booked with ICA representatives or insurers and will take place on Thursday 20 January 2022 from 9am – 8pm.

The decision to hold virtual rather than in-person consultations was made by the ICA and insurers to ensure participant safety due to the current Covid environment. Using technology gives storm affected policyholders the opportunity to discuss the progress of their claims now rather than waiting until the current situation eases.

Bookings are essential for the 30-minute virtual consultations with ICA representatives and insurers. To book go to Catastrophe 214: Victorian Severe Storms & Flooding - Insurance Council of Australia or insurancecouncil.com.au/VicStormsJune21

Insurers have received more than 32,000 claims from the Insurance Catastrophe that was declared on 13 June 2021, with losses estimated at $281 million. More than 90 per cent of claims are from householders for storm and water damage.

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

The Insurance Council of Australia has made the decision to offer individual virtual consultations based on the health and safety of all participants. Virtual face-to-face policyholder meetings are not practice and ICA representatives and insurers would prefer to meet in person with policyholders at community events. However, the current Covid environment has necessitated this move to meet the needs of those policyholders who need assistance with their insurance claim sooner rather than later.

Insurance disaster responders move into South Australia

Insurance disaster responders move into South Australia

News release

Friday, 5 November 2021

Insurance disaster responders are entering South Australia from today to assist with the assessment, management and resolution of claims following last week’s hailstorms, the Insurance Council of Australia (ICA) said today.

The storm cell, which hit areas in South Australia from the Yorke Peninsula through Adelaide, across the Victorian border to east of Melbourne and as far south as Tasmania, has been declared an Insurance Catastrophe by the ICA.

The declaration of an Insurance Catastrophe serves to escalate and prioritise the insurance industry’s response for affected policyholders.

To date 59,237 claims have been lodged across the three impacted states with approximately two thirds of claims in South Australia related to damage to motor vehicles while in Victoria 90 per cent of claims relate to homes.

The ICA has this week worked with the State Government to facilitate the entry of insurance disaster responders into South Australia while border restrictions with New South Wales and Victoria remain.

The 21 specialists being deployed include assessors, loss adjusters and claims specialists. In line with the insurance sector’s Covid-19 Disaster and Recovery Deployment Plan these workers will be subject to a range of restrictions and requirements when in South Australia, as well as being fully vaccinated against Covid-19.

The deployment of insurance disaster responders from interstate is necessary because there are not enough local claims specialists or trades to meet the needs of those impacted by the storm.

With border restrictions still in place while natural disasters are more likely, the ICA has written to national and state leaders calling for a nationally consistent approach to the deployment across state and territory borders of insurance disaster responders.

Insurers are advising that disruption to building supply chains related to the pandemic continue to cause ongoing delays to the supply of building materials nationally.

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

Families, businesses, and communities rely on insurance disaster responders from interstate in the aftermath of natural disasters – without them, recovery is delayed with significant personal, social, and economic impacts.

Modelling undertaken for the Insurance Council found that if an event the size of 2017’s Cyclone Debbie occurred now and insurers were delayed by border restrictions by seven days, a total economic shortfall of $687 million would result over the eight weeks following the event.

The ICA appreciates the efforts of the SA Government, Health and Police to enable the deployment of insurance disaster responders to support the recovery of storm-impacted South Australians.

However, the fact that it has taken more than a week to obtain this approval shows the urgent need for a nationally consistent approach that allows insurers to meet the needs of customers faster.