Insurers look forward to working with new Crisafulli Government

News release

Sunday, 27 October 2024

The Insurance Council of Australia (ICA) today said insurers look forward to working with the new Crisafulli Government to better protect Queenslanders from the impacts of extreme weather.

Queensland is Australia’s most extreme weather-exposed state: around 75 per cent of all Australian homes in cyclonic wind regions are located in Queensland and it has the largest number of properties at risk of flood of any state or territory.

Last month the ICA published A Stronger Queensland, which outlined the policies needed to ensure Queenslanders remain protected and secure.

Analysis included in the report found that at least 310,000 Queensland properties – or around 10 per cent of all Queensland properties – are exposed to a 1-in-100, 1-in-50, or 1-in-20 risk of flooding each year, with at least 47,000 of these properties exposed to the highest 1-in-20 annual risk of flooding.

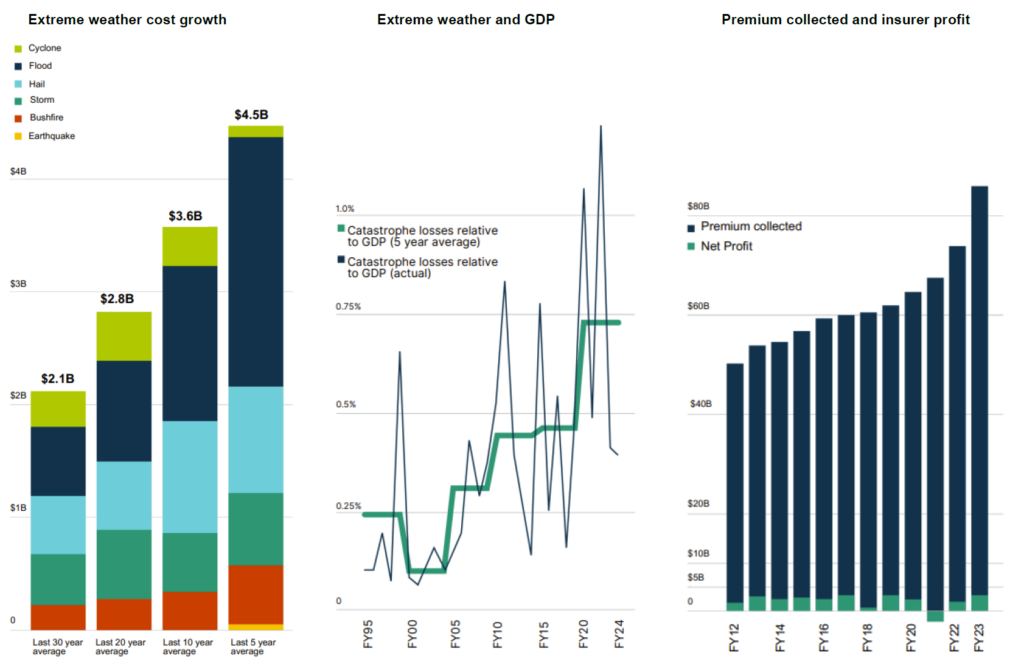

In the last three years insurers have incurred around $4.5 billion in extreme weather claims in Queensland.

The key insurance priorities for Queensland are:

- Reducing the cost of insurance by removing the nine per cent stamp duty paid on insurance policies

- Defending critical infrastructure, including homes and businesses, by substantially increasing funding to better protect against flood and cyclone

- Future proofing the State by stopping development on flood plains and making new homes more resilient to extreme weather

- Supporting the most vulnerable in the community with programs that reduce risk and put downward pressure on the cost of insurance.

Queenslanders could see an immediate reduction in their premiums if the Crisafulli Government removes stamp duty on insurance, which would provide immediate cost of living relief and encourage greater take-up of insurance at a time when it is needed most.

In the current financial year, Queenslanders are forecast to pay $1.7 billion in stamp duty on their insurance policies, up from just over $1 billion in 2019-20.

Quote attributable to Andrew Hall, CEO, Insurance Council of Australia:

The Insurance Council congratulates Premier-elect David Crisafulli and his team on their election victory yesterday and look forward to working with the new Government on our shared priorities of making Queensland safer and insurance more available.

The most immediate way to reduce insurance premiums in Queensland is abolishing the nine per cent stamp duty on insurance premiums.

If the Crisafulli Government does not abolish stamp duty on insurance, it should invest the revenue collected by this tax in mitigation initiatives that directly benefit Queenslanders and put downward pressure on insurance premiums.

Analysis undertaken for the ICA shows that a five-year, $730 million investment in mitigation projects across Queensland would deliver $6.3 billion in savings to 2050 – a nine-fold return on investment.